#EndAusterityNow… or should we?

Thousands of people have gathered in London today to protest against government cuts.

Starting outside the Bank of England, and finishing outside the Houses of Parliament, the rally intends to make the government rethink its austerity-focused economic strategy.

After the global economic crisis of 2007-08, the Conservatives made the decision to reduce government spending, in a bid to reduce the deficit. However, it is argued that this has had a hugely detrimental impact on economic growth.

An Oxfam report, titled ‘The true cost of austerity and inequality‘ states that “economic stagnation, the rising cost of living, cuts to social security and public services, falling incomes, and rising unemployment have combined to create a deeply damaging situation in which millions are struggling to make ends meet.”

The report goes on to say that “just one example among many is the unprecedented rise in the need for emergency food aid, with at least half a million people using food banks each year.”

Foodbanks continue to grow in popularity, a symbol of ever-expanding UK poverty.

In addition, these cuts have had a dramatic effect on numerous public services; despite pledges in the Conservative Party’s 2015 manifesto, the NHS continues to struggle under a tight economic squeeze. The education system is also under threat, with rumours circling of another increase in tuition fees.

This leaves us with a big question: are these austerity measures really working?

On the surface, it would appear that the answer is no. Today’s anti-austerity rally is strong evidence of the UK public’s distaste for government cuts. Supporting this are the public sector strikes we’ve seen in the past five years, most notably in November 2011 and July 2014 (both over pensions, pay and budget cuts).

Moreover, many would argue that the austerity measures have restricted economic growth, rather than encouraging it. Large cuts to government spending can lead to a fall in nominal GDP; an example of this would be Greece in 2011, who saw a 6% drop in GDP, meaning that there was less money available to help pay off the debt.

However, when an economy is so fragile, especially in an instance where national debt is so high (e.g. UK or Greece), increased government spending can have dangerous consequences.

Common sense dictates that if you’re in debt, this is not a good idea.

Austerity measures are typically used for one single purpose – cut down government spending in order to pay off national debt. The reason that this is such an issue is that, if national debt becomes too high, then the entire country can face economic meltdown, with a national market failure.

This is exactly what has happened in Greece; national debt reached €320bn, a figure which they were simply unable to repay, because the Greek government spent all of their money on public sector wages and the pension scheme.

By contrast, the UK national debt is £1.56 TRILLION.

In support of this,economist Tejvan Pettinger says that the primary motive behind austerity is “the morality that the government shouldn’t be spending money they don’t have.”

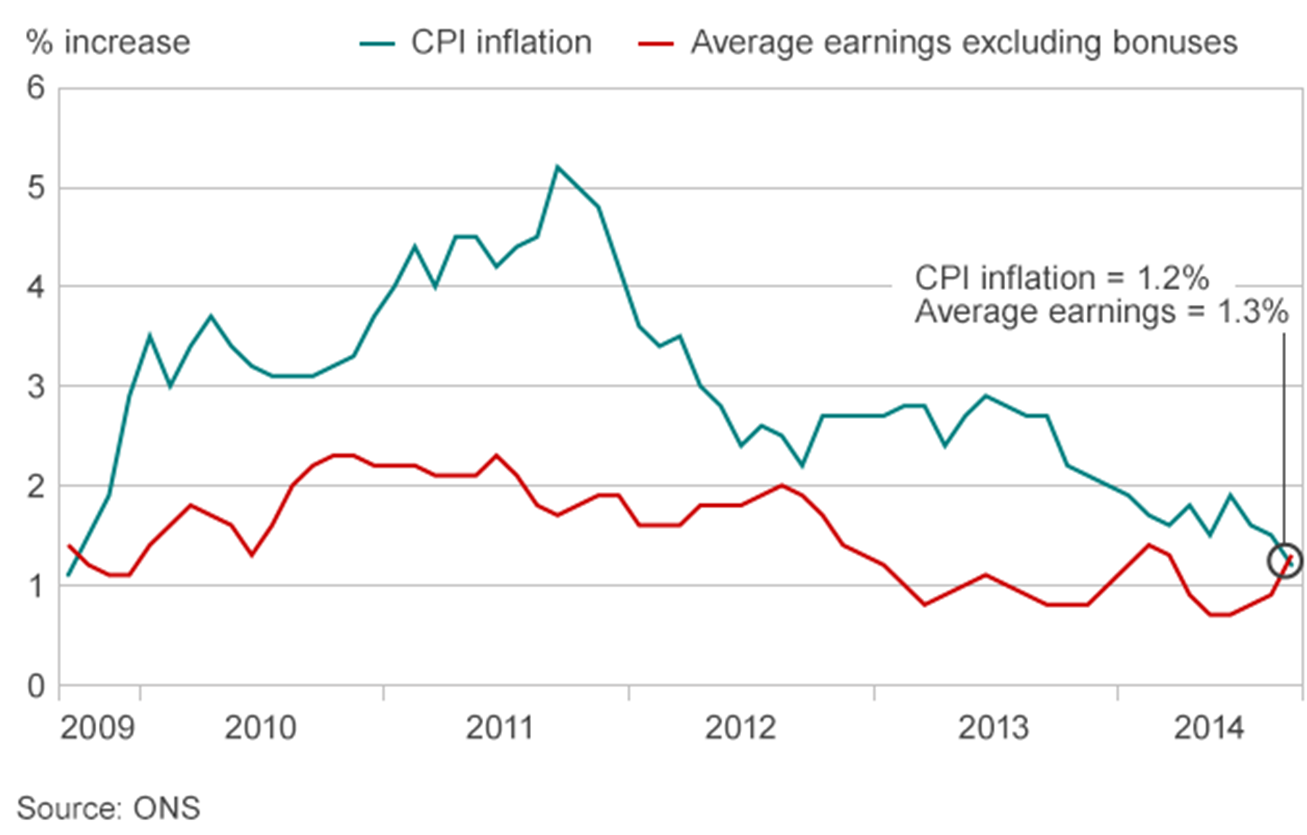

Furthermore, we must take into account the fact that the UK economy is now growing at a steady rate. Since 2010, we have only had 2 quarters of negative economic growth, wages are continuing to rise and unemployment is at it’s lowest in seven years (1.83 million).

Nobody can dispute the fact that austerity is squeezing everyone’s pockets, and it’s unfortunate that those who are slightly worse off are suffering the most. However, with the future of the economy still hanging in the balance, it’s probably the best option; the lesser of two evils, if you will.